1 hour ago

24

1 hour ago

24

When your best-performing holdings become so dominant that portfolio rules force you to dump them, you know the market has entered strange territory. That is exactly what happened to Sam Konrad, the investment manager for Asia Equity Income at Jupiter Asset Management.

On June 8, Konrad revealed that his fund has been compelled to sell its positions in TSMC, Samsung, and MediaTek, three of Asia’s most important semiconductor companies. The reason: the AI rally has made these stocks so large within regional benchmarks that holding them violates the portfolio concentration limits that govern actively managed funds.

The numbers behind the forced selling

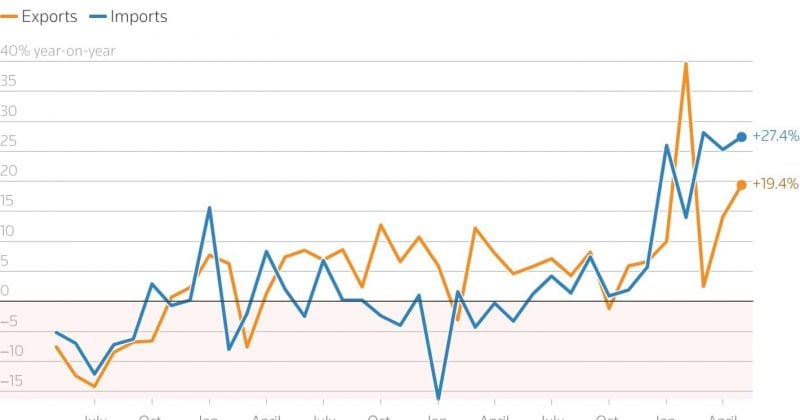

The year-to-date performance of these three chipmakers tells the story. TSMC is up 52%. Samsung has surged 159%. MediaTek has climbed 184%.

TSMC, Samsung, and SK Hynix now comprise almost one-third of the MSCI Asia Pacific ex-Japan Index. In local markets, the distortion is even more extreme. TSMC alone accounts for 41.5% of Taiwan’s TAIEX index. Samsung and SK Hynix together represent 55% of South Korea’s KOSPI.

“We have been forced sellers of TSMC, Samsung and MediaTek,” Konrad stated.

Konrad’s fund strategy allocates nearly half of its assets to Taiwan and South Korea, with MediaTek previously serving as the largest position. The selling was mechanical, not philosophical.

Asia’s own Magnificent 7 problem

US markets spent much of 2023 and 2024 grappling with the “Magnificent 7” phenomenon, where a small number of tech leaders grew so large that the S&P 500 became a de facto tech fund. Asia is now experiencing its own version of that same structural issue, concentrated almost entirely in the semiconductor supply chain. A single company commanding 41.5% of an entire national stock index distorts capital allocation, risk management, and performance benchmarking for every fund operating in the region.

South Korean equities have experienced significant outflows as investors reassess the risks of holding positions in markets where two companies account for more than half the benchmark weight.

Passive funds have been a major driver of this concentration spiral. Approximately $510 billion has flowed into Asian markets over the past five years. A quarter of that total, roughly $127.5 billion, arrived in just the last six months.

What this means for investors

Active managers who are constrained by portfolio rules become natural sellers of the most popular stocks at precisely the moment when passive flows are pushing those same stocks higher. When three companies account for a third of a major regional index, any correction in the semiconductor cycle would hit the benchmark with disproportionate force.

Active managers are increasingly looking at smaller AI-adjacent companies further down the supply chain, including packaging firms, testing equipment makers, and component suppliers that benefit from the same AI infrastructure buildout without carrying the same benchmark weight problems.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.

English (US) ·

English (US) ·