3 months ago

41

3 months ago

41

The post Best Bitcoin & Crypto-Backed Loan Platforms in 2026 appeared first on Coinpedia Fintech News

Unlock liquidity from your crypto holdings without triggering a taxable sale; here’s how the top platforms compare.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Always consult a qualified professional before making financial decisions.

Why Borrow Instead of Sell?

For long-term Bitcoin holders, selling is often the worst option. It triggers capital gains tax, removes future upside exposure, and can be psychologically costly after years of conviction holding.

Crypto-backed lending solves this. You deposit Bitcoin or other crypto as collateral, receive cash or stablecoins, and keep your position intact. When you repay, your collateral comes back. The market now spans centralized platforms (CeFi) and smart contract protocols (DeFi), each with meaningfully different risk profiles.

Platform Types at a Glance

| Type | How It Works | Best For |

| CeFi | A company holds your crypto and manages the loan | Simplicity, fiat loans, customer support |

| DeFi | Smart contracts manage everything on-chain | Lower rates, no KYC, full transparency |

The 6 Best Crypto-Backed Loan Platforms

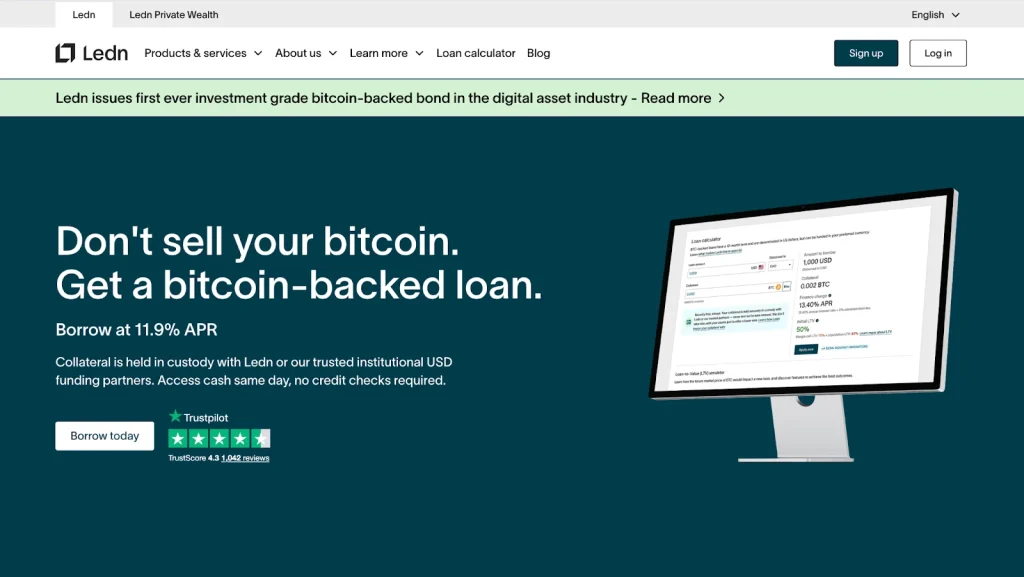

1. Ledn — Best for Bitcoin Holders Who Prioritise Security

Platform type: CeFi | Collateral: BTC | Borrow: USD, USDC, local fiat | Rate: From ~9.99% | Max LTV: 50%

Founded in 2018, Ledn has processed over $10.5 billion in Bitcoin-backed loans without a single reported loss of client funds, a track record that survived the collapses of Celsius, BlockFi, and FTX.

Its Custodied Loan product holds collateral in segregated on-chain addresses, ring-fenced from the platform’s other activities. Neither Ledn nor its funding partners can lend out your collateral for interest, directly addressing rehypothecation concerns. A monthly Open Book Report and independent Proof of Reserves audits every six months add further transparency.

Ledn’s core borrowers tend to be financially sophisticated, long-term BTC holders managing significant Bitcoin wealth. For this profile, trust and track record outrank rate optimisation. Ledn’s 24/7 operations are also a genuine advantage: Bitcoin’s sharpest moves often happen on weekends, when traditional finance is unavailable.

The B2X product lets conviction holders borrow against BTC to buy more BTC instantly. Auto Top-Up automatically adds collateral when LTV hits 70%, reducing liquidation risk.

Trade-off: Rates are higher than DeFi, and the 12-month fixed term is less flexible than open-ended protocols.

Key stats: $10.5B+ loaned | Zero client losses | 6-hour funding | No monthly payments | 100+ countries

2. Aave — Best for DeFi-Native Users with Multi-Chain Portfolios

Platform type: DeFi | Collateral: 120+ ERC-20 tokens | Borrow: Any supported token | Rate: Variable | Max LTV: Up to 82%

Aave is the gold standard for decentralised lending, deployed across 18 blockchains with no KYC and no company holding your funds. Rates move based on pool utilisation, making it well-suited for short-term borrowing windows. Flash loan functionality attracts advanced traders, though it’s not relevant for most borrowers.

Key stats: Battle-tested across multiple market cycles | Ethereum, Arbitrum, Polygon, Base, and more | No origination fees

3. Nexo — Best for Borrowers with Diverse Crypto Holdings

Platform type: CeFi | Collateral: 100+ assets | Borrow: USD, USDC, USDT, fiat | Rate: 11–19% | Max LTV: 90%

Nexo accepts over 100 cryptocurrencies as collateral, including altcoins most lenders won’t touch, with instant approval and 24-hour funding. Tiered interest rates are available to NEXO token holders.

Risks and considerations: Accessing Nexo’s best rates requires holding significant NEXDC token exposure, adding market risk unrelated to your loan; token depreciation can outweigh any interest savings. In 2023, Nexo settled with the U.S. SEC and multiple state regulators for $45 million over unregistered securities allegations, subsequently exiting the U.S. market. New York imposed a five-year ban on Nexo in the securities industry. Nexo discontinued Proof of Reserves reporting after its U.S. exit, with no plans to reinstate it. The platform also accepts its own token as collateral, a structural conflict of interest worth considering.

Key stats: Widest collateral acceptance in CeFi | Unlimited loan duration | No current Proof of Reserves reporting

4. Compound — Best for Ethereum-Native Borrowers Who Prefer Governance Transparency

Platform type: DeFi | Collateral: Major ERC-20 tokens | Borrow: ETH, USDC, USDT | Rate: Variable | Max LTV: Asset-dependent

One of DeFi’s original protocols, Compound sets rates algorithmically and governs changes via COMP token holders, with all decisions visible on-chain. Rates can be competitive during low-utilisation periods but spike under high demand. A solid choice for Ethereum-native users who don’t need fiat output.

Key stats: Fully decentralised governance | Long track record | No origination fees

5. Arch Lending — Best for Institutional Borrowers

Platform type: CeFi | Collateral: BTC, ETH | Borrow: USD | Rate: Negotiated | Max LTV: ~50%

Arch operates at the institutional end of the market (minimum loan sizes from $75,000+), offering dedicated relationship managers and custom loan structuring for complex borrower situations, including trusts, LLCs, and family offices. Rates are negotiated rather than published upfront.

Key stats: Purpose-built for large borrowers | Accommodates investment structures | Relationship-managed service

6. Morpho — Best for Users Seeking Competitive DeFi Rates

Platform type: DeFi | Collateral: Any ERC-20 token | Borrow: Any supported token | Rate: Variable | Max LTV: Variable

Morpho matches lenders and borrowers directly where possible, allowing both sides to benefit from better rates than shared pool models. When no direct match exists, it falls back to standard mechanisms. Its Morpho Blue engine powers 190+ markets and underpins Coinbase’s borrowing product.

Risks and considerations: Borrowing against BTC on Morpho requires wrapping it into WBTC or cbBTC first, introducing custodial and bridge risk; depending on your jurisdiction, the wrapping itself may constitute a taxable event. Smart contract vulnerabilities are a genuine concern across DeFi: a rounding error combined with an access control flaw in Balancer V2 (November 2025) led to estimated losses of over $100 million. Morpho’s permissionless market creation broadens the potential attack surface. Liquidations are automated and instant, often liquidating more collateral than the minimum necessary, with no human review and no legal recourse in the event of failure.

Key stats: Peer-to-peer rate matching | 190+ markets | No origination fees | No regulatory oversight or Proof of Reserves

Platform Comparison

| Platform | Type | Collateral | Rate | Max LTV |

| Ledn | CeFi | BTC only | From ~9.99% | 50% |

| Aave | DeFi | 120+ ERC-20 | Variable | 82% |

| Nexo | CeFi | 100+ assets | 11–19% | 90% |

| Compound | DeFi | Major ERC-20 | Variable | Asset-dependent |

| Arch Lending | CeFi | BTC, ETH | Negotiated | ~50% |

| Morpho | DeFi | Any ERC-20 | Variable | Variable |

Key Risks to Understand

In CeFi: You’re trusting a company with your assets. Platform insolvency, rehypothecation, and regulatory risk are the main concerns. Ledn’s Custodied Loan explicitly prohibits collateral lending; most other CeFi lenders do not.

In DeFi: Smart contract exploits can cause irreversible losses with no recourse. Variable rates can spike. Wrapping BTC introduces additional custodial and potential tax risk. Liquidations are automated and aggressive compared to regulated CeFi models.

Frequently Asked Questions

Is a crypto-backed loan a taxable event? In most countries, no; borrowing against crypto is not a disposal. Local rules vary, and wrapping BTC for DeFi may be treated differently. Always confirm with a tax professional.

What happens if I can’t repay? The platform sells your collateral to recover the outstanding balance. You keep the original loan proceeds.

What’s a safe LTV to target? Below 35% is widely recommended. It provides a meaningful buffer against price declines before approaching liquidation thresholds.

This article is for general informational purposes only and does not constitute financial, legal, or tax advice. Past performance is not a guarantee of future results. Always conduct your own research and consult qualified professionals before making financial decisions.

English (US) ·

English (US) ·