2 hours ago

10

2 hours ago

10

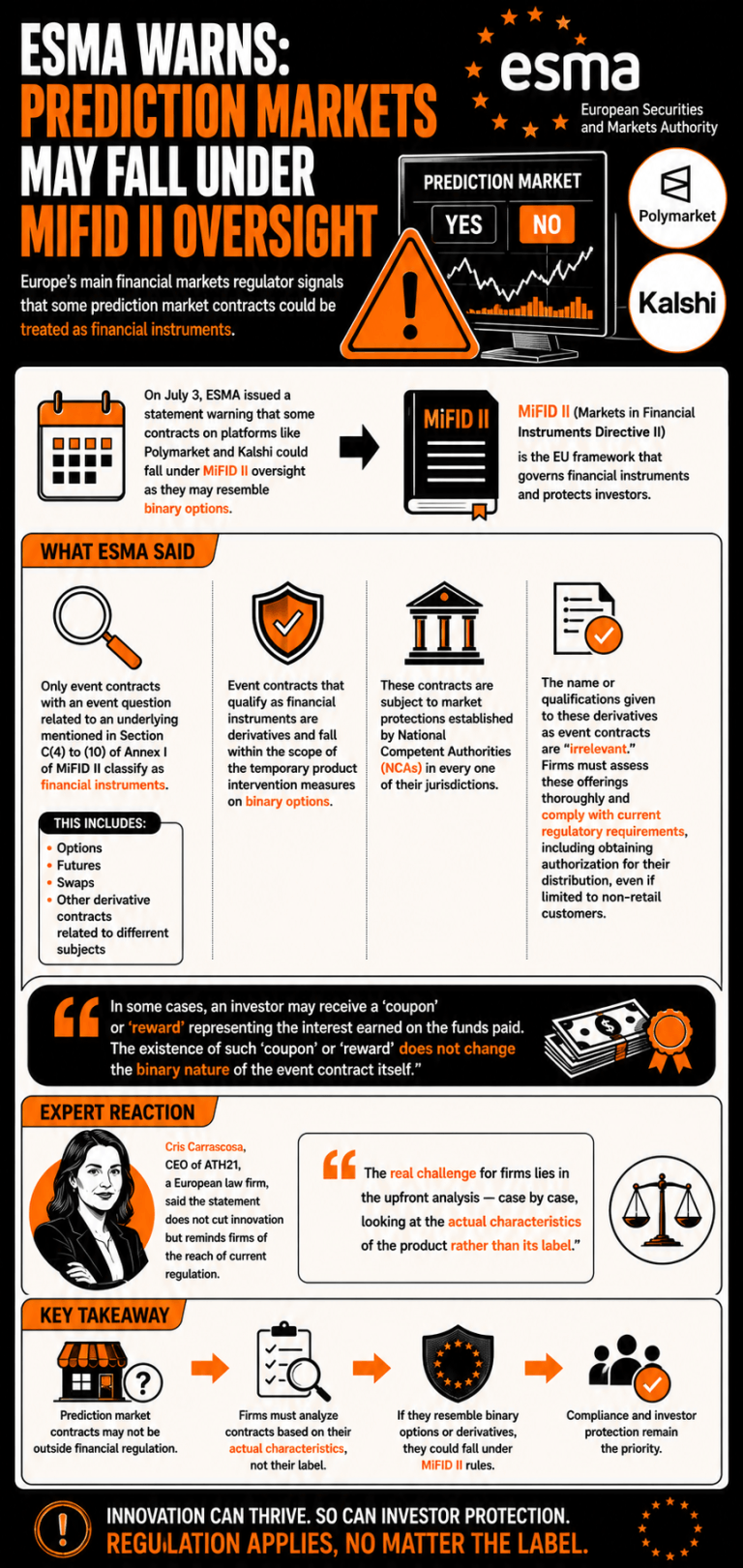

On July 3, ESMA issued a statement warning that some event contracts resembling binary options could fall under current derivatives regulation. The regulator stressed that firms offering these instruments should assess whether these contracts fall under this classification to comply with regulatory requirements.

Published: Jul 6, 2026, 1:30 AM

Key Takeaways

- ESMA warned prediction contracts may act as binary options, forcing platforms to seek MiFID II approval.

- Regulators declared event contract labels irrelevant, subjecting them to national market protection rules.

- European law experts urged firms to analyze products case-by-case to guarantee regulatory compliance.

Europe Puts Its Sights on Binary Options-Like Event Markets

The European Securities and Markets Authority (ESMA), Europe’s main financial markets regulator, has issued a statement warning about the application of current regulatory frameworks to some contracts offered in prediction markets.

On July 3, ESMA stressed that some contracts offered on prediction market platforms such as Polymarket and Kalshi could fall under MiFID II (Markets in Financial Instruments Directive II) oversight, as they might resemble binary options.

The regulator stated that “only event contracts with an event question related to an underlying mentioned in Section C(4) to (10) of Annex I of MiFID II classify as financial instruments,” which include options, futures, swaps, and derivative contracts related to different subjects.

ESMA declared that event contracts that qualify as financial instruments “are derivatives and fall within the scope of the temporary product intervention measures on binary options,” and are subject to market protections established by National Competent Authorities (NCAs) in each of their jurisdictions.

The name or qualifications given to these derivatives as event contracts are “irrelevant,” ESMA claimed, and the firms offering them should conduct a thorough assessment of these offerings and comply with current regulatory requirements, including obtaining authorization for their distribution, even if limited to non-retail customers.

“In some cases, an investor may receive a ‘coupon’ or ‘reward’ representing the interest earned on the funds paid. The existence of such ‘coupon’ or ‘reward’ does not change the binary nature of the event contract itself,” ESMA concluded.

Cris Carrascosa, CEO of ATH21, a European law firm, highlighted that the statement did not cut innovation but rather reminded firms of the reach of current regulation. “The real challenge for firms lies in the upfront analysis —case by case, looking at the actual characteristics of the product rather than its label,” she assessed.

English (US) ·

English (US) ·