1 hour ago

19

1 hour ago

19

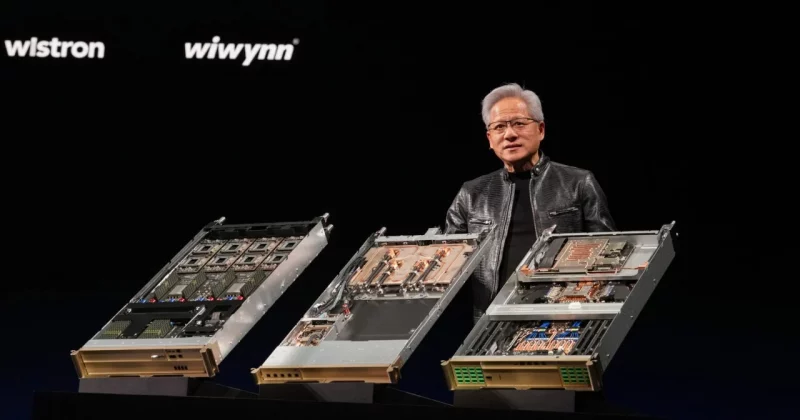

The company that built its empire assembling iPhones now makes more money from AI servers. Hon Hai Precision Industry, better known as Foxconn, posted a 34% year-over-year revenue increase for the April-to-May 2026 period, pulling in NT$1.69 trillion ($53.6B). That figure beat analyst expectations of 32% growth.

The driving force behind the surge is straightforward: hyperscalers and cloud providers are spending aggressively on Nvidia-powered AI infrastructure, and Foxconn is the one building the servers. AI servers now account for roughly 40% of the company’s Cloud and Networking Products segment revenue, making them a larger contributor than the smartphone assembly lines that defined Foxconn for decades.

The numbers behind the AI pivot

May was particularly strong. Revenue jumped 40% month-over-month, suggesting that demand is accelerating rather than plateauing. April had already shown momentum with approximately 30% year-over-year growth.

The first quarter of 2026 set the stage for this performance. Foxconn reported over 29% revenue growth and a 19% profit increase in Q1, establishing a clear trajectory heading into the second quarter.

Foxconn has responded to this momentum by raising its full-year 2026 revenue target to NT$11 trillion ($350.5B). That represents a 36% increase for the year. The company also expects AI server rack shipments to more than double over the course of 2026.

Why Foxconn owns this market

Foxconn currently holds over 40% of the global AI server market. Foxconn is positioned as a key manufacturing partner for Nvidia’s upcoming Vera Rubin generation of AI supercomputing platforms. When cloud providers like Microsoft, Google, and Amazon place their next round of massive infrastructure orders, Foxconn will be the company that actually turns those purchase orders into physical hardware.

What this means for investors

For Nvidia, Foxconn’s growth validates the demand narrative that has powered its own stock price. Every Foxconn server rack shipped represents Nvidia GPUs deployed, networking equipment installed, and recurring workloads that will eventually need upgrades.

Foxconn’s expectation that AI server rack shipments will double implies sustained capital expenditure from hyperscalers throughout 2026. That’s bullish for the entire supply chain: memory manufacturers, power management companies, data center REITs, and cooling technology providers all stand to benefit from this level of infrastructure spending.

The risk to watch is concentration. When 40% of your fastest-growing segment depends on one chip architecture from one supplier, any disruption to Nvidia’s roadmap, whether from supply chain issues, export controls, or competitive threats from AMD and custom silicon, could create turbulence. Foxconn’s bet on Vera Rubin is a bet that Nvidia maintains its dominance in AI training and inference hardware for at least the next product cycle.

The other variable worth monitoring is whether the AI infrastructure spending cycle has staying power or whether it’s front-loaded demand that will cool once the initial buildout phase ends. Foxconn’s aggressive NT$11 trillion revenue target for 2026 assumes that spending continues at this pace for the rest of the year, and any pullback from major cloud customers would make that number much harder to hit.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.

English (US) ·

English (US) ·