4 hours ago

21

4 hours ago

21

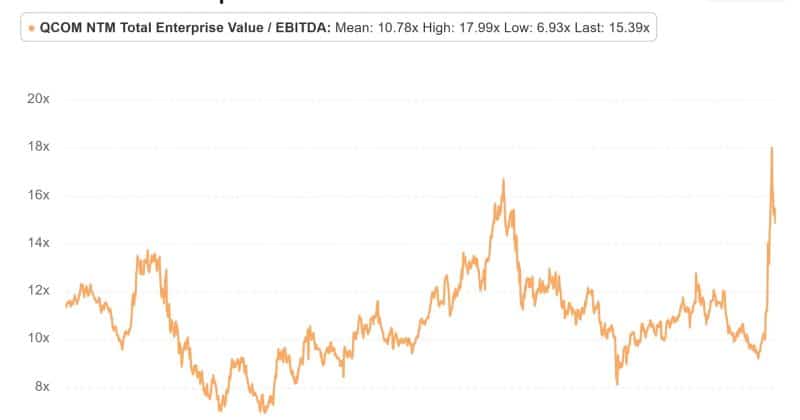

Qualcomm just made its most credible move yet into the Qualcomm AI data center market — and Wall Street noticed immediately. Shares jumped 15% in extended trading after the chipmaker unveiled a multigenerational CPU deal with Meta, introduced a new AI inference architecture, and nearly doubled its non-handset revenue forecast for fiscal 2029. For a company still widely associated with smartphone chips, the announcements signal a genuine pivot in progress.

Key takeaways

- Qualcomm announced a multigenerational CPU deal with Meta to supply processors for its next-generation server fleet, with production starting in 2028.

- The company has secured two major hyperscale customers, with only Meta publicly identified; together they are expected to generate at least $1 billion in revenue within a year.

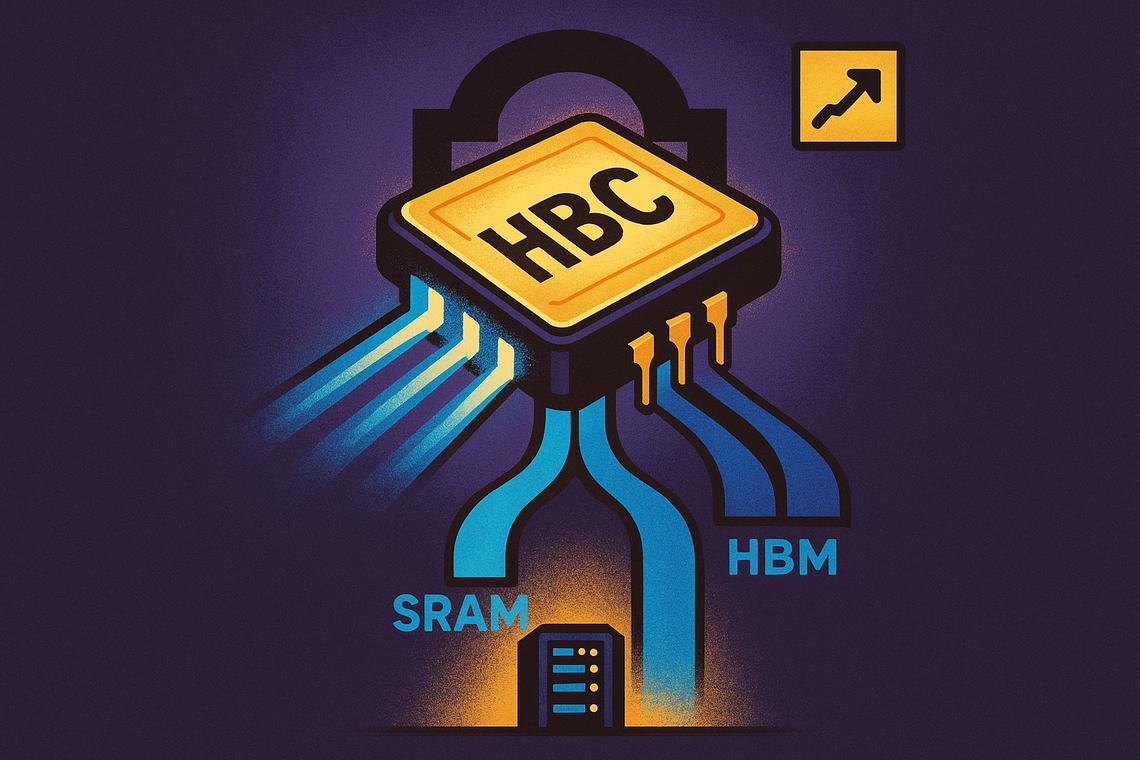

- Qualcomm introduced High-Bandwidth Compute (HBC), a new AI inference server architecture designed to reduce memory bottlenecks by combining SRAM-class performance with HBM-class capacity.

- The company raised its fiscal 2029 non-handset revenue projection to $40 billion, up from a prior forecast of $22 billion, with data center alone targeting over $15 billion.

- Qualcomm’s acquisition of Modular strengthens its open software stack, positioning it as an Nvidia CUDA alternative across heterogeneous silicon architectures.

Qualcomm’s Multigenerational CPU Deal with Meta

The centerpiece of Qualcomm’s Investor Day was a direct endorsement from one of the world’s largest AI spenders. Meta CEO Mark Zuckerberg announced the partnership in person, describing it as a multigenerational agreement in which Qualcomm will supply CPUs for Meta’s next-generation server fleet starting production in 2028.

“Our goal is to deliver personal superintelligence to everyone in the world,” Zuckerberg said. “That’s why our work with Qualcomm is so critical.”

The specifics — processor names, deployment timelines, exact workloads — were not disclosed by Meta. What was made clear is that this is not an exclusive or wholesale replacement of Meta’s existing silicon strategy.

Meta’s Portfolio-Based AI Infrastructure Strategy

Meta described its infrastructure approach as deliberately diversified. A company spokesperson said Meta is “embracing a flexible, portfolio-based approach, combining hardware from a range of partners with our own rapidly advancing MTIA silicon program.” In plain terms: Qualcomm CPUs will complement, not replace, Meta’s in-house chip development.

That distinction matters for understanding the scale of the opportunity. Qualcomm becomes one node in a broader Meta hardware ecosystem, alongside Meta’s own MTIA accelerators and other third-party suppliers. It’s a partnership, not a monopoly position — but for Qualcomm, even a share of Meta’s server buildout represents meaningful revenue at hyperscale volumes.

Securing Major Hyperscale Customers and Market Validation

Meta is not the only win. Tony Pialis, Qualcomm’s Executive Vice President and General Manager of Data Center, confirmed the company has secured two major hyperscale customers. “We have won two major hyperscaler deals that will contribute meaningful revenue to Qualcomm, starting at the end of this year,” he said. The second customer has not been publicly named.

CFO Akash Palkhiwala added that the two customers combined are expected to generate at least $1 billion in revenue within a year — a concrete near-term benchmark that gives investors something to track.

Endorsements and Market Recognition

Beyond Meta, Microsoft CEO Satya Nadella appeared at the event and endorsed Qualcomm’s High-Bandwidth Compute architecture. He stopped short of announcing any commercial deployment, so the endorsement functions more as market validation than a confirmed contract.

Industry analyst Matt Kimball, Vice President and Principal Analyst for Data Center Technologies at Moor Insights & Strategy, offered a measured read on what the Meta deal actually means for the broader server CPU market. “One customer win doesn’t change the server CPU market overnight,” he told Data Center Knowledge. “But it definitely expands the conversation.” He added that the deal gives Qualcomm both the revenue to fund continued product development and the credibility to pursue additional cloud customers — a compounding effect that matters more over time than any single contract.

Palkhiwala also noted that Qualcomm already has existing business relationships with nearly every major hyperscaler through its smartphone and edge chips. “This is not a new relationship,” he said, framing the data center push as a natural extension of trust already built, rather than a cold-start sales effort.

Introducing the High-Bandwidth Compute (HBC) Architecture

Qualcomm’s technical centerpiece is High-Bandwidth Compute, a new AI inference server architecture that combines SRAM-class performance with HBM-class capacity. The goal is straightforward: eliminate the memory bottleneck that increasingly limits how fast large AI models can run inference workloads.

Technical Goals and Innovation

The company’s broader data center chip lineup now includes a CPU called the Dragonfly C1000 — the processor Meta will deploy starting in 2028 — designed specifically for agentic AI with an emphasis on compute performance at lower power consumption. Qualcomm argues that its long experience building energy-efficient chips for smartphones gives it a structural advantage as hyperscalers run into power limits in their data centers.

No performance benchmarks or detailed technical specifications were released for HBC at the event.

Potential Impact on AI Inference Workloads

Kimball sees HBC as potentially one of Qualcomm’s most significant technology announcements, conditional on execution. “If Qualcomm delivers what it’s describing, HBC could improve both inference performance and efficiency, particularly in disaggregated AI infrastructure where moving data efficiently is often as important as adding more compute,” he said.

That caveat is worth noting. The AI chip market rewards demonstrated performance, not architectural promises. Qualcomm will need to show production data before HBC’s real competitive weight can be assessed.

Qualcomm’s Broader AI Data Center Platform and Revenue Outlook

Rather than betting everything on a single chip, Qualcomm is presenting itself as a full-stack infrastructure supplier. The company’s data center platform spans CPUs, AI accelerators, networking, custom silicon, and an open software stack. That last element — software — was reinforced by Qualcomm’s acquisition of Modular, a startup whose technology enables AI applications to run efficiently across different chip architectures. Qualcomm positions Modular as comparable to Nvidia’s CUDA, but architecture-agnostic.

Comprehensive Product Portfolio

Pialis made the strategic framing explicit: “Traditional infrastructure will not scale to the needs of agentic AI. The industry needs a paradigm shift.” Whether that pitch lands with additional hyperscalers depends on whether Qualcomm can demonstrate it delivers across all layers simultaneously — not just on one chip in one customer’s fleet.

Kimball pointed to the software acquisition as a potentially important differentiator. If operators can run AI workloads efficiently across multiple silicon architectures using Qualcomm’s software, the company becomes stickier in an infrastructure environment that is growing more heterogeneous by design.

Financial Projections and Growth Strategy

The financial targets that drove the stock surge are ambitious by any measure. Qualcomm now projects more than $40 billion in non-handset revenue by fiscal 2029, nearly double its prior forecast of $22 billion. Data center alone accounts for more than $15 billion of that total. The company is also targeting $10 billion from automotive and more than $14 billion from IoT, with handsets dropping to roughly one-third of chip revenue under that scenario.

Palkhiwala explained the mechanics behind the data center growth path: “There really isn’t enough supply, and multiple players are needed.” Kimball echoed the logic from a market structure perspective. “Hyperscale economics are different than enterprise infrastructure. A relatively small number of large customer wins can translate into billions of dollars of annual revenue very quickly.”

CEO Cristiano Amon pushed back directly against the narrative that Qualcomm is a latecomer. “When people ask about if it’s late to enter the data center, you should think about scale and execution, or engineering capabilities, or operations and supply chain,” he said. The implicit argument: Qualcomm’s manufacturing scale, existing hyperscaler relationships, and chip design expertise are assets that don’t have an expiration date.

The harder question is whether $15 billion in data center revenue by 2029 requires two hyperscale customers or twenty. With one named, one unnamed, and the rest of the market still watching, the gap between the projection and the pipeline is where the real execution risk lives — and where the next investor day will likely be judged.

FAQ

What is the significance of Qualcomm’s CPU deal with Meta?

The multigenerational CPU deal marks a major validation moment for Qualcomm’s data center ambitions. Meta will use Qualcomm’s Dragonfly C1000 CPU in its next-generation server fleet starting production in 2028, making Meta one of the first major hyperscalers to publicly commit to Qualcomm silicon for AI infrastructure.

How does Meta integrate Qualcomm CPUs in its AI infrastructure?

Meta uses a portfolio-based approach that combines Qualcomm CPUs with hardware from multiple partners and its own MTIA silicon program. Qualcomm CPUs complement rather than replace Meta’s in-house chip development efforts.

What is Qualcomm’s High-Bandwidth Compute architecture?

High-Bandwidth Compute, or HBC, is Qualcomm’s new AI inference server architecture. It is designed to reduce memory bottlenecks during inference workloads by combining SRAM-class performance with HBM-class capacity. No performance benchmarks have been publicly disclosed yet.

What revenue targets has Qualcomm set for its data center business?

Qualcomm expects more than $15 billion in annual data center revenue by fiscal 2029, as part of a broader projection of over $40 billion in total non-handset revenue — nearly double its previous forecast of $22 billion.

Article produced with the assistance of artificial intelligence and reviewed by the editorial team.

English (US) ·

English (US) ·